At Airlie, we look to invest in quality companies that we believe are undervalued by the market. Often these opportunities emerge when a great business sits within an otherwise mediocre sector, or when the market assigns an arbitrary discount to a type of business. For us, Seven Group Holdings (SVW) falls into both categories.

Seven is a conglomerate of industrial businesses. Two of these businesses sit in sectors often unloved by investors for their volatile returns and capital intensity – mining services (WesTrac) and equipment rental (Coates). Furthermore, in listed equities ‘conglomerate’ is a dirty word. It can imply complexity, opacity and bloat, where the corporate structure of the company sits at odds with interest of the shareholders, and many investors choose to avoid conglomerates for these reasons. In our mind, WesTrac and Coates are quality businesses sitting within mediocre industries, pushed further out of sight by the conglomerate structure of Seven. While investors digest the highly publicised on-market takeover of Boral or lament the decline of the namesake Free To Air TV business (Seven West Media), WesTrac and Coates quietly demonstrate their quality and form the majority of our valuation of Seven.

WesTrac – Less cyclical than it appears?

WesTrac is the authorised Caterpillar dealer in Western Australia, New South Wales and the Australian Capital Territory, providing heavy equipment sales and support to customers. Caterpillar employs an independent dealership sales model for its heavy machine sales and support services. Caterpillar thinks this model fosters a stronger relationship between dealers and local customers (acknowledging the importance of high-quality after-sales service and support) and allows Caterpillar to focus its capital allocation on product development and innovation.

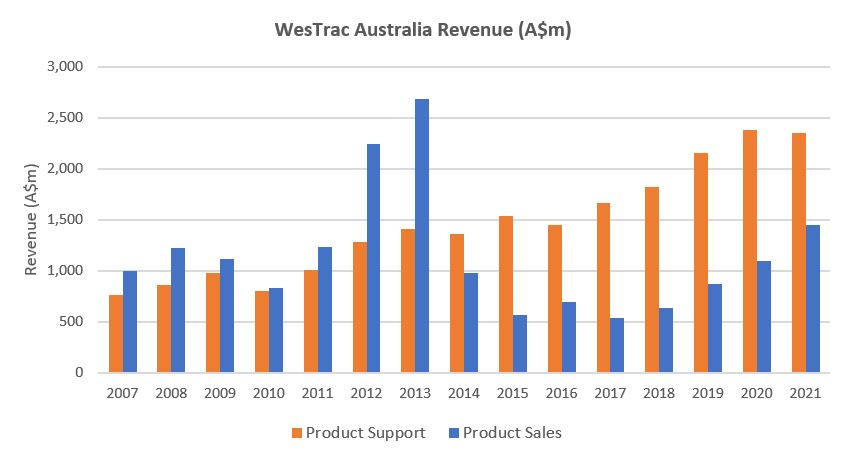

WesTrac sales are given in two segments – product sales (i.e. machine sales) and product support. Product sales have been reasonably cyclical, tied to future production volumes and the fleet replacement cycle of the tier-1 and tier-2 miners (and at a second derivative, commodity prices and miner profitability). Product support sales have been far more steady, growing at a 10-year rate of 7.0%, as new sales enter the maintenance program and old equipment sees parts intensity increase and its life extended.

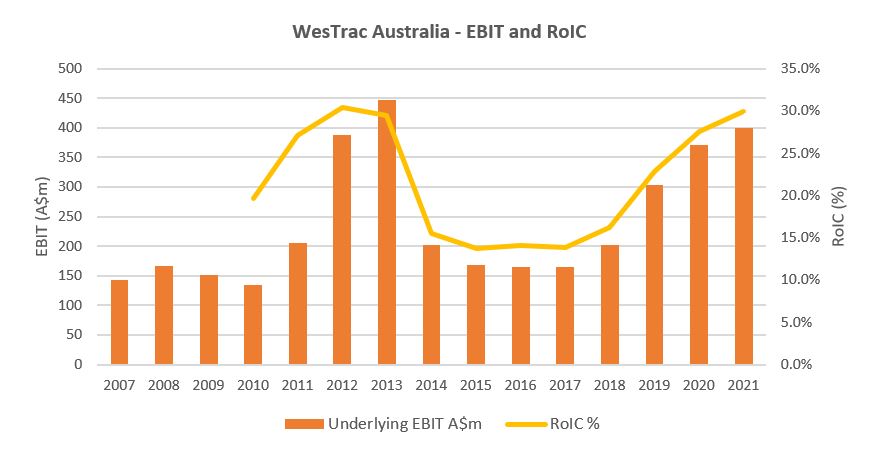

Through the cycle, WesTrac has had a return on invested capital ranging from about 14% (2015, 2016) to 30% (2012, 2021) and EBIT margins between 7% to 11%.

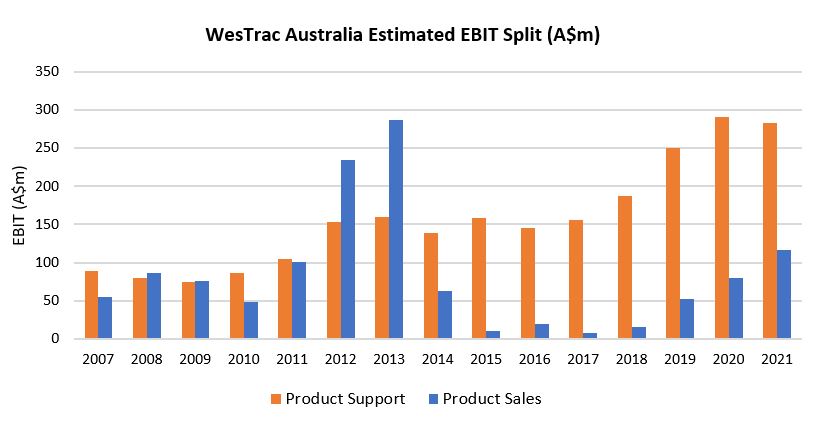

WesTrac does not disclose earnings by segment, but our analysis suggests the earnings of the business have shifted materially towards product support over the past decade. Given product-support revenue is more predictable and still growing, this should mean that even if new sales decline the earnings of the business is more sustainable (versus a decade ago) with arguably a higher ‘mid-cycle’ earnings base.

Finally, Caterpillar has an internal target of doubling its revenue from product services (via the dealership network) by 2026, as it looks to take advantage of fleet-replacement cycle extensions and expanded product lifecycle offering.

The net of this is that we believe WesTrac is far less cyclical than typical mining-services businesses, and earns stronger returns through the cycle, and should be valued as such.

Coates – Impressive transformation ahead of a revenue inflection?

Coates Hire is Australia’s largest general equipment hire company and provides a range of general and specialist equipment to a variety of markets including engineering, building construction and maintenance, mining and resources, manufacturing, government and events. The business is primarily exposed to east coast infrastructure, industrial and residential projects, as well as resources activity.

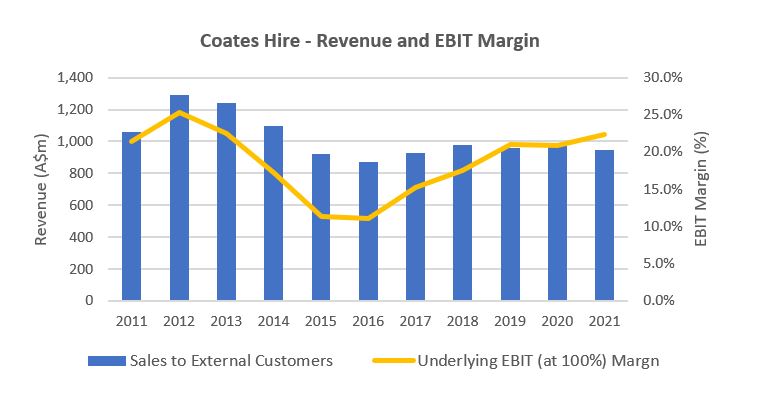

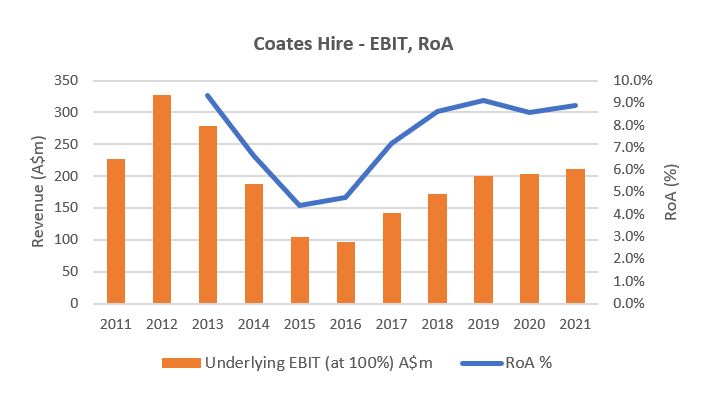

The Coates business is thriving. Following the resources boom earlier in the decade, Coates’ margins slumped from about 25% to about 11% as revenue fell from about A$1.3 billion to A$870 million (-32%) from FY12 to FY16. Management has since undertaken a material cost-out, transformation program that has been delivered incredibly successfully:

- In FY15, Coates delivered A$104 million of EBIT on A$919 million of revenue (11.4% margins). In FY21, on essentially flat revenue (A$946 million), Coates delivered A$212 million of EBIT (22.4% margins).

- Since FY15, EBIT has grown at a CAGR of 12.5%, while revenue growth has been benign at a CAGR of 0.5%.

For FY22, management has guided to high single-digit EBIT growth. Looking further out, management is driving the business towards the internal ‘Team25’ project goals. Team25 is a continuation of the existing transformation strategy within Coates with the business targeting A$1.25 billion of revenue and a 25% EBIT margin. Part of the success of the Team25 targets will rely on revenue growth driven from increased market share and east coast infrastructure spend, however cost-out initiatives still form part of the strategy. Were management to successfully execute on the Team25 targets, Coates would deliver about $313 million of EBIT, versus A$212 million in FY21 (+48% overall, or a 10% CAGR to FY25).

The takeaways for us are two-fold:

- First, Coates management has built an impressive track record of cost management and margin growth in a benign revenue environment; and

- Second, given the above, Coates should see material operating leverage in its earnings should revenue start to grow.

Coates’ margins and returns sit in the top-quartile of the global equipment rental sector, and there remains the potential for considerable earnings growth over the next two to three years (on top of that delivered steadily since 2016). Both of these factors suggest to us that the business is of higher quality than most would expect of typical rental equipment companies.

Valuation

Of course, Seven does not just consist of WesTrac and Coates. Within the conglomerate also sit stakes in listed companies Boral (70%), Beach Energy (30%) and Seven West Media (40%), as well as unlisted energy, media and property holdings. Of these investments, the recently acquired 70% stake in Boral is the most material (and where valuation is arguably most up for debate). Including the Boral investment, we estimate Seven is trading on a P/E multiple of sub 14x FY22 earnings, which is a about a 25% discount to the S&P/ASX 200, and in our mind an undemanding valuation.

In our ‘sum of the parts’ analysis of the business, we see upside to the current share price when taking a more mid-cycle view of the earnings of WesTrac and Coates, and before including any material valuation upside to the Boral business, should management successfully execute the transformation program and unlock additional value in the non-core property portfolio. Finally, our confidence in the conglomerate structure comes back to ownership. Seven remains 60% owned by the Stokes family, with Kerry Stokes in the chairman role and his son Ryan as CEO. In our view this gives shareholders significant alignment with the board and management, and we have found that through time founder-led businesses tend to consistently outperform the broader index.

Sources: Company filings and website

By Joe Wright, Airlie Investment Analyst